Install the Valley West Mortagage Mobile App for free today

and begin your path to owning a home.

Copyright 2026 Valley West Corporation DBA Valley West Mortgage. All Rights Reserved. NMLS #65506 | #VEGASSTRONG. This site is protected by Google reCaptcha and the Google Privacy Policy and Terms of Service apply.

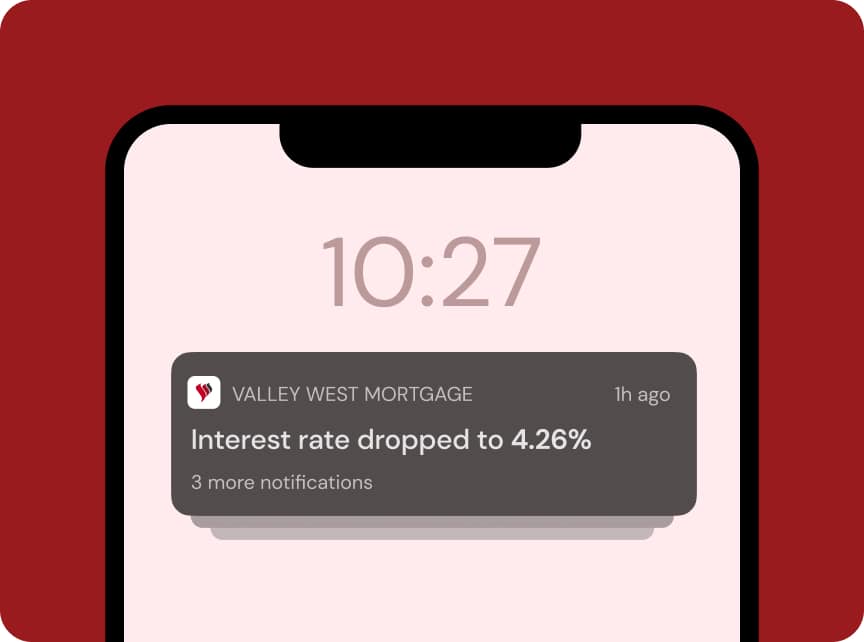

Instant notifications for your scenario

Let's do it⏰ Your offer will be delivered to your inbox in less than a minute!